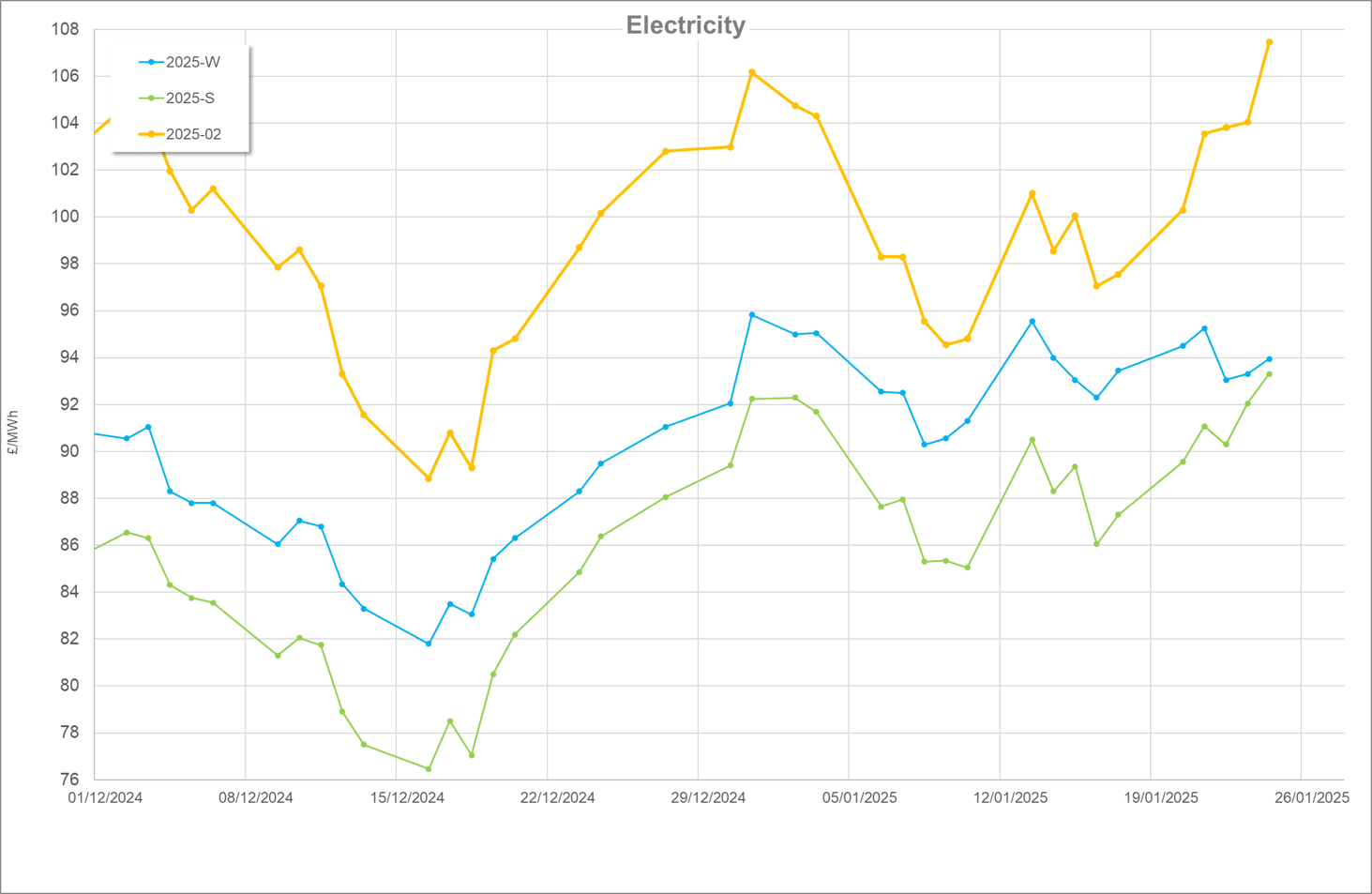

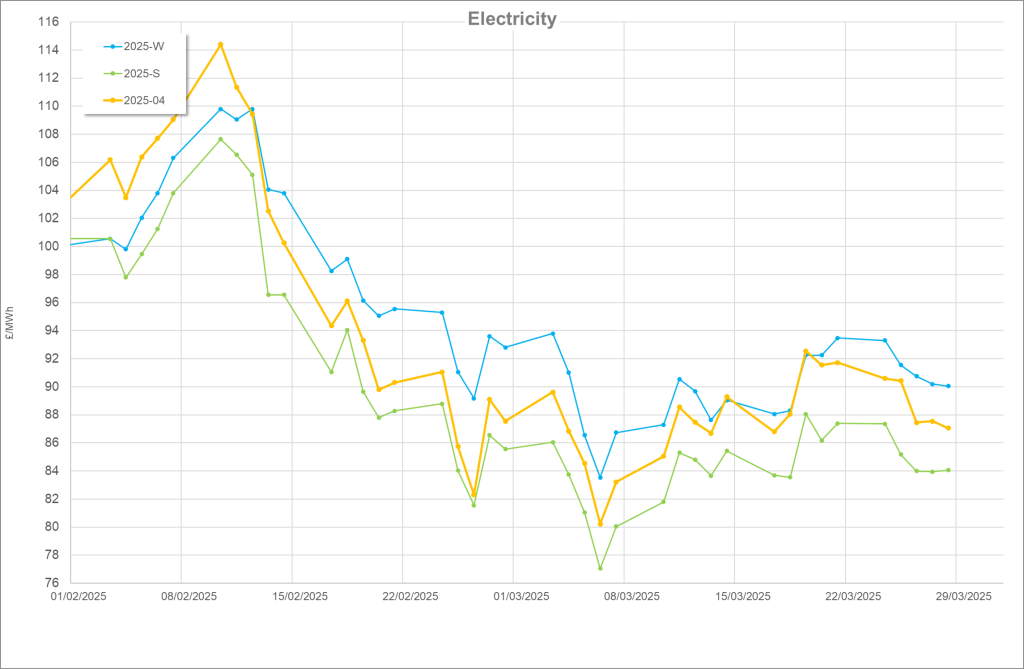

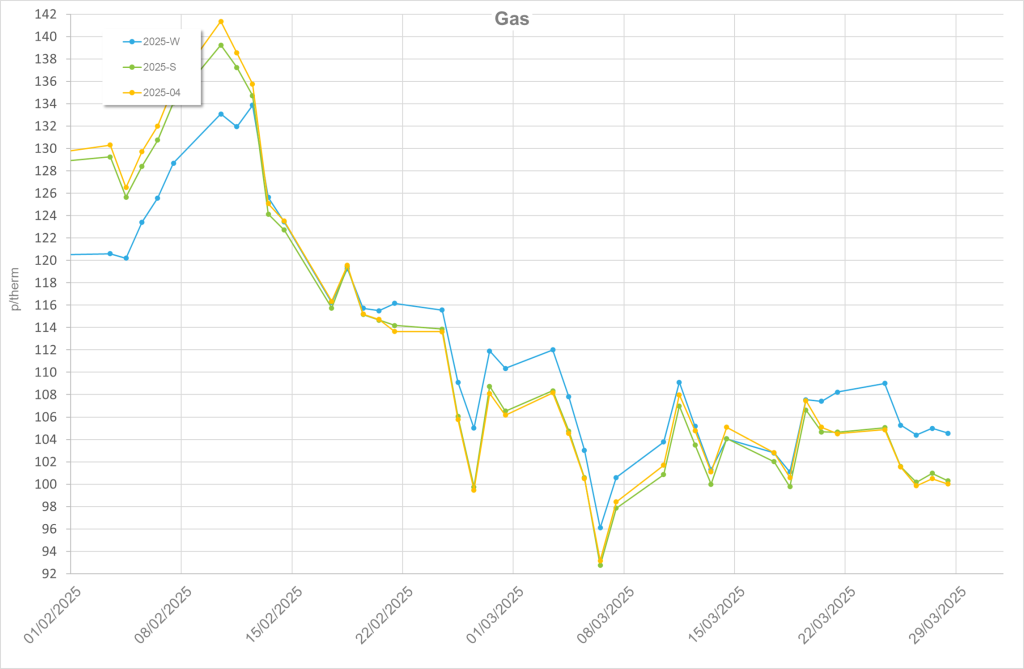

February Recap

February saw a mix of conditions in both gas and power pricing. The first 10 days saw sharp price rises with continued momentum from January. Prices then swiftly decreased, settling back to levels seen in mid-December before the price hikes. Three main factors drove these price increases:

Firstly, the fall out of Donald Trump’s inauguration for his second stint in the Oval Office had the markets on edge. His bold decrees and some of his cabinet choices made the markets nervous. Particularly of note was his threats of sanctions on Iran which had a similar effect to the Houthi rebel attacks in the region >12months prior. Although the inauguration was in January, Trump’s global tariff threats continued to add to the price rises before dissipating throughout the month as the initial shock began to wear off.

Secondly, gas storage in Europe reached the lowest points since the energy crisis. Large parts of the month saw weather under seasonal averages which did not help storage injections either as consumers relied on more gas for heating, breaking away from more frugal habits since 2022. This was exacerbated when the markets seemingly struggled to recover from the shock of the last Russian gas into Europe ending on 31st December. Several EU nations appealed to the regulators about future targets, claiming that economic conditions to fill through Q1 were challenging. It was shortly after this action that saw the prices start to erode indicating the markets were somewhat placated by potentially evolving storage strategy.

Thirdly, the war in the Ukraine continued to wage, markets still showed nervousness in the situation particularly with energy infrastructure coming under fire. The wearing off of the initial shock of the Trump inauguration, warming weather and the markets finally coming to terms with life after Russian gas in Europe saw a quick drop in pricing. Wind production finished neck and neck with gas for the dominant source of power with both creating 8TWh.

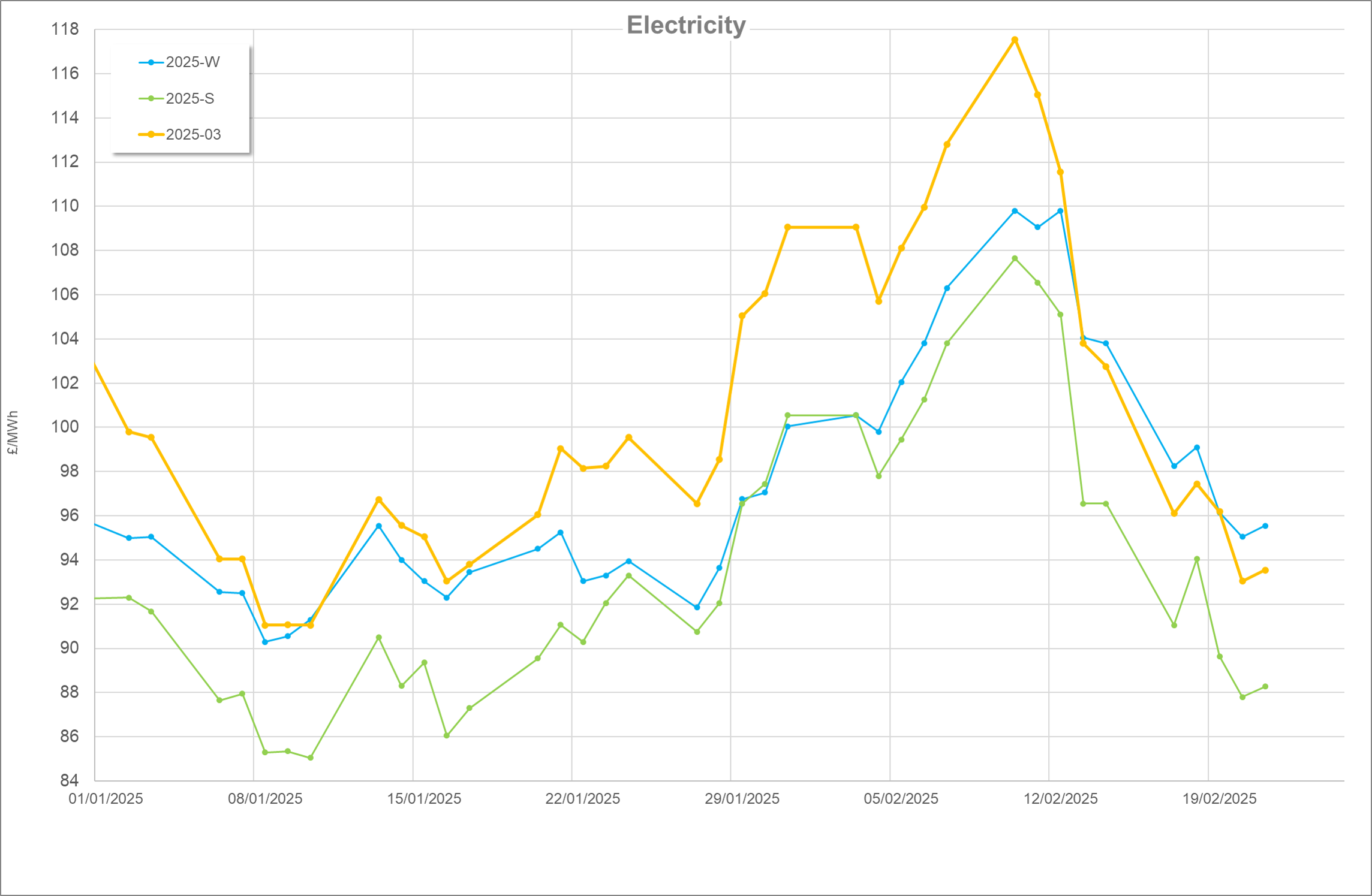

March

Wind generation dissipated into March dropping off to 6.5TWh generated from turbines whereas gas generated 7.69TWh. Considering the turbulent January and February, March’s pricing remained relatively calm. Despite a cooler middle of the month where temperatures again dropped below seasonal averages, the last third of the month stayed consistently warm for the time of year. The beginning of the month too was warm with temperatures building through until the 10th. It is perhaps no surprise that some gas injections into storage on the 7th and 8th encouraged prices to decrease to the lowest point in the last 2 months, however with the aforementioned cool conditions arriving on the 10th and further injections ceasing this was short lived.

The energy news was largely dominated by political conditions regarding Ukraine. 3 years from the initial Russian invasion, Donald Trump tried to instigate peace talks with Russia’s Vladimir Putin. It was frankly a bit of an odd follow. A combative press conference between Trump and Zelensky bridging February and March had commentators worried Trump was “cosying up” to Russia. This was then preceded by initial peace talks not including Ukraine which the Ukraine PM did not respond kindly to. Although during a second wave of talks saw a tentative ceasefire agreed including no further strikes on energy infrastructure, this quickly went by the wayside following explosions at the Sudzha metering station. Ukraine and Russia blamed each other and hostilities seemingly resumed. Trump went on record using some very strong language regard Putins approach to the ceasefire in somewhat of a U-turn from his early month stance. As Winter 24’s trading period came to an end it was interesting to see that prices closed relatively close to their open back in October.

Upcoming

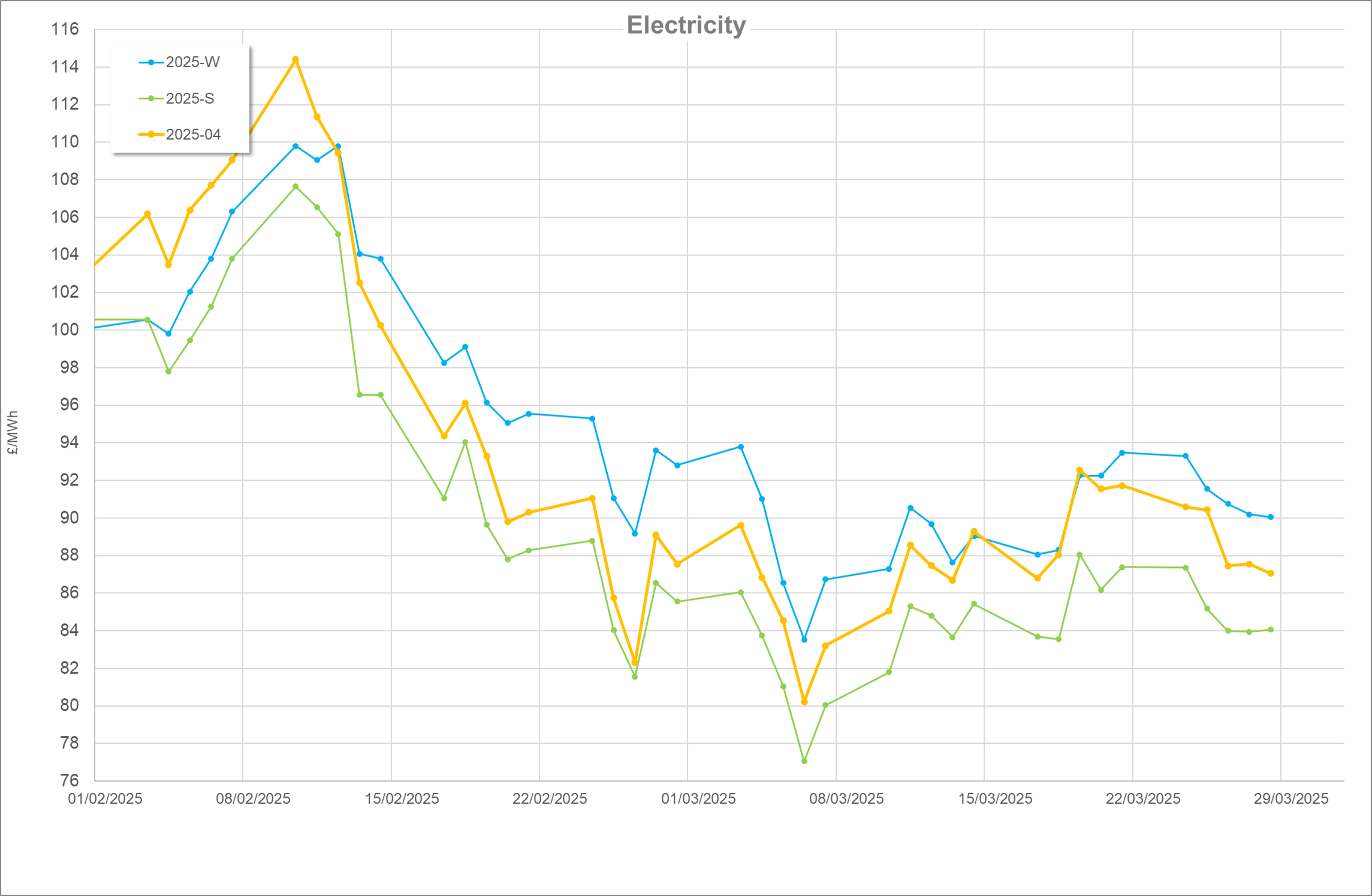

Norwegian Gas Maintenance – this first wave from 3/4/25 is expected and should be anticipated by the markets regarding pricing. However the last 2 years have seen strong gas storage levels ahead of the first wave. The reverse as we saw in Marchs update above is currently true. Should colder temperatures prevail, demand for gas or power be above normal and or any delays to the Norwegian schedule be observed, this could have an adverse effect on prices.

Ukraine – Although Trump is seemingly committed to helping bring peace to the Ukraine it seemingly remains a way off and further developments are hard to predict. It seems also that peace in the Ukraine would present a hurdle for Trump to overcome as Putin will likely want to see sanctions lifted on being able to sell gas to Europe whereas Trumps LNG is seemingly set to fill the void.

Written by Ed Kimberley

Related Content